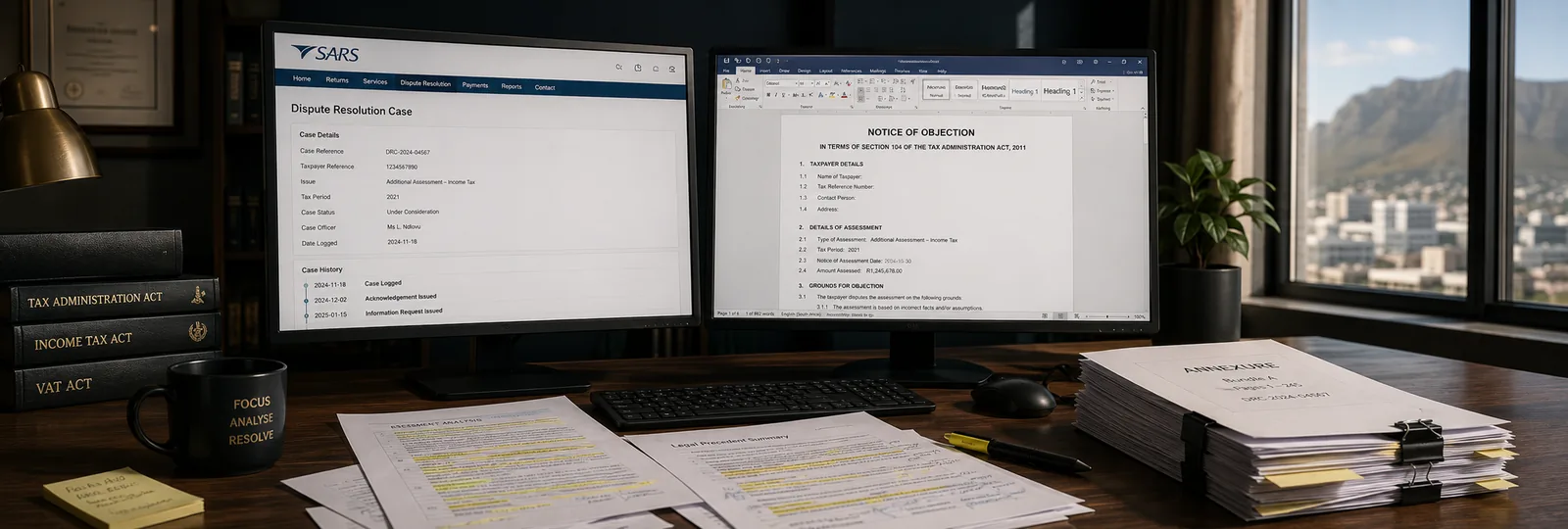

Disagree with SARS? We will take it on.

An additional assessment, a denied refund, a penalty or an understatement finding is not the end of the matter. The Tax Administration Act 28 of 2011 gives you a clear right to dispute it, if you act in time. Send us the letter and we run the process for you, properly documented and SARS-defensible.

If any of these has landed on your desk, bring it to us.

The clock usually starts the day SARS issues the letter. Send it through early and we take it from there.

Additional or estimated assessment

SARS has raised your tax, including section 95 estimates where information was outstanding.

Understatement penalties

Penalties of 10% to 200% under sections 222–223 — often disputable on the behaviour category.

Refund withheld or verified

A refund stopped, a verification or audit, or a request for relevant material.

Admin & late-payment penalties

Fixed-amount and percentage penalties that can often be remitted on the right grounds.

VAT, PAYE & other assessments

Disputes across all tax types, not just income tax.

Section 179 & collection steps

Third-party appointments on your bank account and other collection action.

Disallowed deductions or input VAT

An expense, allowance, exemption or input VAT refused — often recoverable with the right evidence.

Undisclosed income or errors (VDP)

Regularise a past default through the Voluntary Disclosure Programme before SARS notifies an audit.

Hand it to us. We run the whole dispute.

You should not have to learn the Tax Administration Act to deal with SARS. That is our job. You give us the letter and the facts; we build the case and carry it through.

We protect the deadline

We calculate and diarise every business-day deadline, so your right to dispute is never lost to the clock.

We build the grounds

Objections and appeals are won on documentation and the correct legal grounds, set out against the Act and SARS practice.

We fight it through

From objection to ADR, the Tax Board and the Tax Court if needed — and we push SARS when it stalls.

“You should not have to learn the Tax Administration Act to deal with SARS. That is our job.

We chase SARS so you don’t have to.

SARS has its own deadlines and frequently misses them. When it does, we do not simply wait — we escalate on a set schedule, measured in business days past the SARS deadline.

We draft a Complaints Management Office (CMO) complaint and notify you.

We file the CMO complaint and send a senior SARS official escalation.

We file a Tax Ombud complaint, having exhausted SARS’s internal remedies.

Partner review and, where justified, a High Court review under PAJA.

Not every SARS letter is a fight.

A lot of needless cost comes from treating every SARS letter as a full dispute. The first question is what the letter actually is, and the lightest correct response that resolves it. We make that call for you.

Light-touch — most matters

- A verification (IT34V, VAT217, EMP217) is a request for documents, not an assessment. We upload the support on eFiling, usually within 21 business days.

- A simple calculation slip is often fixed by a request for correction or a reduced assessment.

- A first administrative penalty is usually dealt with by a request for remission (RFR01).

Full dispute — the minority

- An additional assessment with a penalty (AP34).

- An understatement penalty under sections 222–223.

- A section 95 estimated assessment.

- A disallowed deduction, input VAT or exemption.

Want to see how it works?

The full dispute process, the deadlines that matter and two free tools — a deadline calculator and a penalty estimator.

A SARS letter on your desk? Don’t wait.

The dispute clock is already running. Send us the letter and we will confirm your deadline, your options and the likely path.